Stock Diversification – what’s the right way? (originally posted in June 2008)

“Through all its vicissitudes and casualties, as earth-shaking as they were unforeseen, it remained true that sound investment principles produced generally sound results. We must act on the assumption that they will continue to do so”. Benjamin Graham in “The Intelligent Investor” published in 1949. The Intelligent Investor was endorsed by Warrant Buffett as “by far the best book on investing ever written”

Benjamin Graham, who is credited with creating the foundation for modern fundamental analysis of stocks, created many well known and widely used theories for investors, including the concept of the ‘margin of safety’, which was aptly termed by Warren Buffett as the 3 most important words in investing.

Why is that? Because the first and foremost guiding rule of value investing is preservation of principal. In order to achieve this, the investor must find companies that are trading at a market price that is a discount to the intrinsic, or real, value. The difference between the market price and the intrinsic value of a stock is what is the margin of safety. Since stock prices tend to fluctuate based on emotions, interest rates, news, reports, and other forces outside the control of the general investor, hence higher the discount, higher is the margin of safety.

An essential element of the margin of safety concept is the principal of diversification. Graham recognized that no investor is perfect in his or her decision making, and unforeseeable market forces can cause unfavorable market turns for an investment even with a margin of safety. Proper diversification of a portfolio offers additional protection against these events.

In the ‘Intelligent Investor’, he wrote, “There is a close logical connection between the concept of a safety margin and the principle of diversification. Even with a margin in the investor’s favor, an individual security may work out badly. For, the margin guarantees only that he has a better chance for profit than for loss – not that loss is impossible. But the more the number of such commitments is multiplied, the more certain does it become than the aggregate of the profits will exceed the aggregate of the losses. That is the simple basis of the insurance-underwriting business”.

But how much diversification is appropriate? And is there complete unanimity on this amongst the modern day value investors?

Warren Buffett, who is certainly Graham’s most famous (and richest) disciple, clearly disagrees with his guru on this aspect.

“Charlie and I decided long ago that in an investment lifetime it's just too hard to make hundreds of smart decisions. Therefore, we adopted a strategy that required our being smart - and not too smart at that - only a very few times. Indeed, we'll now settle for one good idea a year. The strategy we've adopted precludes our following standard diversification dogma.

Many pundits would therefore say the strategy must be riskier than that employed by more conventional investors. We disagree. We believe that a policy of portfolio concentration may well decrease risk if it raises, as it should, both the intensity with which an investor thinks about a business and the comfort-level he must feel with its economic characteristics before buying into it.

I cannot understand why an investor of that sort elects to put money into a business that is his 20th favorite rather than simply adding that money to his top choices - the businesses he understands best and that present the least risk, along with the greatest profit potential. In the words of the prophet Mae West: "Too much of a good thing can be wonderful.” Warren Buffett in his 1993 letter to shareholders.

Many pundits would therefore say the strategy must be riskier than that employed by more conventional investors. We disagree. We believe that a policy of portfolio concentration may well decrease risk if it raises, as it should, both the intensity with which an investor thinks about a business and the comfort-level he must feel with its economic characteristics before buying into it.

I cannot understand why an investor of that sort elects to put money into a business that is his 20th favorite rather than simply adding that money to his top choices - the businesses he understands best and that present the least risk, along with the greatest profit potential. In the words of the prophet Mae West: "Too much of a good thing can be wonderful.” Warren Buffett in his 1993 letter to shareholders.

In another discussion, he said:

“If you are not a professional investor, if your goal is not to manage money in such a way as to get a significantly better return than the world, then I believe in extreme diversification. So I believe 98 or 99 percent, maybe more than 99 percent, of people who invest should extensively diversify and not trade….” “But once you’re in the business of evaluating businesses and you decide that you’re going to bring the effort and intensity and time involved to get that job done, then I think that diversification is a terrible mistake to any degree…. If you really know businesses, you probably shouldn’t own more than six of them. I mean, if you can identify six wonderful businesses, that is all the diversification you need, and you’re going to make a lot of money and I will guarantee you that going into a seventh one, rather than putting more money into your first one, has got to be a terrible mistake. Very few people have gotten rich on their seventh best idea. But a lot of people have gotten rich on their best idea. So I would say that for anybody working with normal capital who really knows the businesses they’ve gone into, six is plenty, and I’d probably have half of it in what I liked best.”

- Warren Buffett at University of FloridaWe therefore have 2 views: one by the original Guru and the other led by a disciple who eventually came out of the Guru’s shadow and became a Guru in his own right.

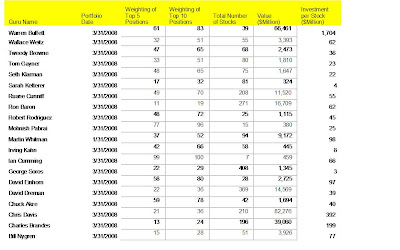

In order to take this forward, we researched on the investment practices of some of the leading names in the US. These are all value practitioners and names that we respect for their investment ideologies.

Of the above list, 5 have investments of more than 50% in the top 5 stocks and 10 have more than 60% in the top 10 stocks.

Warren Buffett, who owns 39 stocks in Berkshire’s $66 billion equity portfolio, has 61% of his investment in his top 5 holdings, more than 83% in top 10 holdings. This is what Charlie Munger said: "Our investment style has been given a name - focus investing - which implies ten holdings, not one hundred or four hundred. The idea that it is hard to find good investments, so concentrate in a few, seems to me to be an obvious idea. But 98% of the investment world does not think this way. It's been good for us."

Mohnish Pabrai likes to have 10 positions equal weighted. Currently he has 13 stocks, with 99.6% of the weighting in top 10.

Others like Bill Nygren of Tweedy Browne, David Dreman and George Soros have 28%, 36% and 29% respectively in their top 10 stocks.

Lets take this forward – diversification, even if done, may mean different things to different people. Many investors hold 50-100 stocks in their diversified portfolio. Some think that the Markowitz model, based on a seminal paper that won Harry Markowitz a Nobel Prize, is the right way to go. This model suggested that investors could reduce their risk by constructing a portfolio of assets with low cross-correlations. Diversification could also mean investing in different industries or different market caps or a combination of growth or value stocks.

Our methodology and its rationale

o We tend to typically start an investment with a size of anywhere from 3-5% of the total investible amount. Value investors very commonly invest early and sell early and hence this strategy, provides us with a foot in the door. We therefore get into a stock which after our due diligence looks interesting but where we may want to wait for the stock to fall further. If it doesn’t fall and instead rises, that’s fine – it’s a nice problem to have. We review our options at that time and may want to exit at a price which we think is an appropriate one.

If on the other hand it falls further, then presuming that in our view the fundamentals of the company have not changed, we may wait for the fall to be atleast 10% from our original price and then pick up another 3-5%.

If on the other hand it falls further, then presuming that in our view the fundamentals of the company have not changed, we may wait for the fall to be atleast 10% from our original price and then pick up another 3-5%.

o In most cases, we would stop averaging down after the stock reaches 10% of the total investible amount. Why?

o We feel that disclosure practices in the country, though along the lines of the developed countries still have some way to go.

o Furthermore, managements of mid-caps may tend to be less transparent in India in comparison to, say, the US (not to say that an Enron can be prevented in the developed world, but generally there is more transparency in those markets).

A cap on the total investment therefore helps us ensure that there is a discipline on the total amount that should be invested on one particular stock.

o Our current feeling is that this limit should apply only at the time of the purchase of the stock and not post purchase. Therefore, if after we have purchased the stock, its price rises and for this reason it becomes higher than 10% of the total portfolio, we do NOT sell some portion of the stock such that it reaches within the 10% cap. Presuming ofcourse that the stock has not reached its sale price as per our expectations.

o Industry caps, we feel, do have a value – we would not for example put all our monies in a Pharma or an IT sector, even though they may look very enticing. Given the overall cap of 10% on a single stock, we feel that having a cap of around 30% on one particular industry may make sense. There is however no logical basis for this cap.

o Overall, we do not expect our portfolio to have more than 30-40 stocks.

Clearly then, there is no one right or wrong way to invest and the investor has to follow what seems appropriate to them though it is agreed that too much diversification is inappropriate just as too much concentration is not right. Each to his own.

No comments:

Post a Comment