“Are We There YET?” (Originally published in November 2008)

In that lovable movie ‘Shrek 2’, Shrek and his wife, Princess Fiona, just back from their honeymoon, are requested to join her Royal parents at the ‘The Kingdom of Far-Far Away’. Reluctant at first, Shrek finally embarks upon the journey alongwith Fiona and their happy-go-lucky partner, The Donkey. They travel night and day through rain, hail and snow. But true to its name, ‘The Kingdom of Far-Far Away’ was REALLY that – far, far away! But, the Donkey is bored with the travel. He keeps asking Shrek: “Are we there yet?” to the point where Shrek is at his wit’s end. So much so that towards the end of the trip Shrek starts asking the same question – Are We There Yet?

Falling profits, plummeting demand, job cuts, and bankruptcies –pretty much all that one gets to read as headlines these days – is making everyone search for clues as to whether the world has reached its economic nadir, the point from where the recovery will start. Are we there yet? There are no clear answers.

Widespread problems and no quick fix visible

What IS clear is that the ongoing crisis has exposed how complicated the world’s financial system has become. No nation or individual has possibly been left untouched. Admittedly, the current turmoil is larger, more complicated, more interconnected and more global than most had anticipated. Even countries, which till just a couple of months back looked like they were sitting pretty on the back of high commodity prices are battling a bubble-bursting experience of their own. At a personal level, youngsters who are starting their careers are just as impacted, as those who have worked for decades.

Meanwhile, the economic indicators continue to disappoint. Consumer spending is down – especially in the US (where it all started and which continues to be the bellwether for world economics), where such spending represents two-thirds of the US’s economic activity. Malls are sporting sale signs, some seven feet tall. And yet sales are dropping. Worse, it is reported that the slowdown has hit luxury chains AS WELL AS stores that sell mass goods, suggesting that consumers at all income levels are snapping their wallets shut.

In consequence of this, there could be another lurking problem. As World Bank chief, Robert Zoellick has mentioned in a post, the current crisis, largely stemming from banking sector problems, will lead to round two: collapsing international trade and the resulting hit on small export-oriented economies. A leading indicator of which is the Baltic Dry Index. (Every working day, the Baltic Dry Index surveys shipping brokers around the world and asks how much it would cost to book various cargoes of raw materials on various routes.) The index has recently fallen to an all-time low (closing at 842 on Friday, November 7) from a high of 15,000 about a year ago. Once trade slows down, some countries' economic growth will be reduced substantially: some East Europeans, some countries in East Asia, and Latin America. This could well lead to more problems with the financial institutions. Scary thought # 1.

According to available data, this is proving to be one of the worst times for funds. In 5 of the last 10 years, fewer than 15 percent of hedge funds had lost money. Even in the worst year, 2002, 31 percent finished down, according to estimates from HedgeFund.net, a unit of Channel Capital Group. This year, some 70 percent of hedge funds had lost money from Jan. 1 through the end of September.

Losers include well-known traders like Kenneth C. Griffin, who runs the Citadel Investment Group; Lee S. Ainslie, head of Maverick Capital; and David Einhorn, the head of Greenlight Capital, who pointed out the troubles at Lehman Brothers before many others.

Pessimism is feeding on itself as managers exchange increasingly gloomy emails about the coming meltdown.

"Be careful buying ANYTHING today," Kyle Bass, managing partner of Hayman Advisors, warned in an Oct. 17 letter to investors. "There will be a time to buy stocks, and that time is a few years into the future when the strong have separated themselves from the week ... a time when unemployment has hit 10% and U.S. GDP has dropped 4-5% (maybe more)."

Seth Klarman, a top-performing value investor and head of The Baupost Group LLC, told clients in an Oct. 10 letter that the economic downturn could be "vicious and protracted." "The financial market collapse and bailout makes us sick," he wrote. "There is likely more carnage to come."

Howard Marks, chairman of Oaktree, a giant LA-based fixed-income hedge fund firm, said some "great" investors he knows were "genuinely depressed" when the credit crisis reached a peak in October.

There is no question that hedge funds are downsizing at present. And a few of the troubled ones have temporarily refused to give investors their money back by freezing their funds. That is NOT the whole story though. The average hedge fund uses leverage, to the tune of about 1.4 times. This is down significantly from a year ago, but it might mean that hedge funds may need to liquidate investments of at least $500-550 billion in order to meet current redemption requests by current year-end. Scary thought # 2.

Collateral Crisis and Governmental Role

Clearly, there’s been no lack of commentary on what’s happened over the last 15 months or so. If we were to summarize it simply: the world enjoyed a strong growth phase in mid 2000s led by global expansion. This encouraged investors (including financial institutions) and consumers to get comfortable with greater leverage – which actually makes some sense in low-volatility environment. For example, it helps boost returns for investors and increases affordability for consumers.

The problem came when there were excesses, which certainly was the case in 2007. As per John Galbraith in his brilliant book called ”A short history of financial euphoria”, “All crises have involved debt that, in one fashion or another, has become dangerously out of scale in relation to the underlying means of payment. There can be few fields of human endeavor in which history counts for so little as in the world of finance”.

These excesses have now resulted in a substantial unwinding process and a collateral based crisis. Specifically, a collateral-based crisis is marked by a devastating positive feedback loop: an asset price drops, leading to a margin call, leading to asset sales, leading to a further drop, leading to another margin call, and so on. Governments can possibly solve liquidity-based crises with injections of liquidity. Collateral crises are much more damaging and prolonged and require substantial natural de-leveraging.

The usual approach towards managing a financial crisis is via the monetary policy – spend more and reduce interest rates. Unfortunately, in a number of countries (like India), there is less maneuverability since they have been attempting to cut their high budgetary deficits for a few years now. Still, some economies like China that have budget surpluses have introduced a fiscal stimulus package worth almost USD 600 bn.

However, in using monetary policy there is a dilemma. If the central banks lower interest rates to mitigate liquidity pressures, there is a possibility that the currency might depreciate further. This may likely lead to a run on a few currencies with further implications on the financial sector. Scary thought # 3.

Some of the emerging economies and in particular the East European economies do not have adequate forex reserves. Hence, economies like Hungary, Romania and Denmark have actually had to RAISE interest rates to prevent currency depreciation. Iceland had lowered interest rates on 15 October 2008 from 15.00% to 12.00% but reversed its decision on 28 October 2008 to raise its rates from 12.00% to 18.00%!

Furthermore, the governments can only attempt to push further liquidity through banks and financial institutions. But globally it has been reported that financial institutions had about $5 trillion of tier-one capital on the eve of the credit crisis. Those in the United States and European Union had about $3.3 trillion of tier-one capital supporting a loan book of some $43 trillion. As per a report, if we apply mark-to-market rules, global financial sector losses are estimated to amount to 85% of tier-one capital. Hence, we can expect these institutions to be just a wee-bit reluctant to lend for a while despite the friendly nudges from the Government.

Lastly, as Governments move to kick-start their economies by spending more, they would need to increase their issuances of Treasury Bills, causing a flood of paper with attendant risks and less than adequate returns on such paper.

Philosophy

Clearly a lot can go wrong. But for a moment lets remove all the intricacies and try to understand this situation with a bit of Philosophy. (We tend to agree with the Hungarian central bank governor András Simor who In a WSJ interview, said recently: In today's world you need a psychologist and not an economist to understand markets.)

With a sense of Déjà vu (we wrote some of the following lines in our very first write-up), we’d like to mention that there’s no gainsaying that humans learn everything through imitation. They are either influenced by someone’s company or they put someone as their ideal and follow them, making progress or taking inspiration from them. It has been found that infants begin mimicking facial expressions within one hour after birth, and we go on imitating words, faces, body language, styles of dress, so¬cial fads, and fashions until we die. In fact in a number of experiments it has been shown that people in a conversation do not merely mimic the dominant conversationalist, but mimic simultaneously, including accent, speech rate, vocal intensity, pauses, and quick¬ness to respond. If the dominant person talks loudly, everybody else also tends to bellow.

Doing exactly what everybody else is doing, no matter how dumb it may look to outsiders, is ingrained in all beings. We have this subconscious feeling that if we aren't doing what everybody else is doing, then its not a good thing. Chickens who have eaten their fill begin to eat again when they are placed with a hungry chicken who is pecking voraciously at a pile of grain. Ants work harder when paired with other worker ants.

And humans? Despite our vaunted individualism, we are the most imitative animals on earth. We mimic the shot of our favorite cricket player or the expression of our favorite actor. We even laugh more when there is a laugh track. This is described as the “Social Proof”.

Another interesting aspect is what has been described as the “negativity bias”. As per this, it is our biological nature to accentuate the negative, to notice the one dumb thing that goes wrong rather than five or ten things that go right. We differentiate between negative and positive events in just a tenth of a second, and the negative ones grab our attention.

For Instance, when researchers show test subjects a paper with a grid of smiley faces on it and one angry face, the test subjects instantly zero in on the angry face. Reverse the pattern, and it takes them much longer to pick out the solitary smile. An angry face would tend to grab our attention more urgently than many smiley faces because it represents a potential threat.

Negativity bias also helps explain why we suffer exaggerated fear of economic loss but experience relatively little emotion about profit. We remember Black Monday from 1987 and even Black Thursday from 1929. But, where is White Wednesday or Bright Friday? Banished from memory.

Perhaps the above 2 principles can somewhat explain the economic cycles. After all, there are times when there is extreme exuberance in the economy and in such times, more investment, capacity addition and large M&As are almost a norm. A business head not doing so is almost made to feel like they are from another planet. Such new investment stimulates demand, producing economic growth, which in turn reinforces confidence, which then results in even more investment. Eventually, confidence gives way to overconfidence and overcapacity. And as the boom wears on, firms tend to take on more and more unnecessary costs. Executives get jets for their personal use; armies of personnel are built within silos. As a result somewhere below the glowing surface of the economy, efficiency suffers.

And sure enough, there are other times when people are evermore hesitant to invest (this is more vivid now!). This too is contagious. And when enough firms choose to wait, the economy falls into a depression creating serious hardships for much of society. Eventually, things become so bad that even a string of good news is quickly discounted. Like in Shrek 2, the honeymoon gets over and so begins the traverse through the difficult conditions in search of the kingdom of far-far away. Where presumably everything will be OK once again. But this too changes and the whole cycle repeats all over again.

So, Are we there YET??

There are many who have recently ventured to answer the question “Are we there yet?” Most have been downright despondent but here we mention one of Peter Drucker's ideas wherein he suggested that accepting what everybody knows without any examination would often result in faulty decisions. This is the backbone of the Contrarian theory of investment as well.

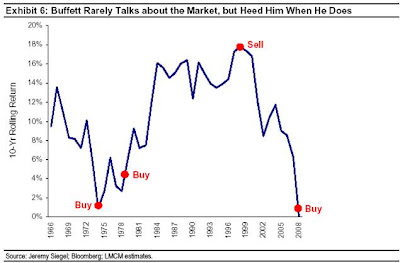

So instead, we quote from a fund manager’s letter who is more positive – a rarity these days. Mentioning that Mr. Buffett rarely takes the initiative to comment on the markets, this writer mentions of the instances when he has made the exception: “In the 1999 article, within 4 months of the market’s top, he (Buffett) suggested that real returns from the market going forward were likely to be about 4%, and if he was wrong, he thought his number was likely too high. In the past decade, we’ve (US markets) been very close to a zero real return.

“In October 2008, he wrote that “the market will move higher, perhaps substantially so, well before either economic sentiment or economy turns up”. Exhibit 6 plots Buffett’s market calls on the rolling 10 year returns. He has proven to be reliably prescient.”

In our own little view, we believe that the crisis may not be over yet by any means and worse may still be ahead. However, depending upon everyone’s individual ability to put aside some money for the future, one should look at picking up some of the great investments, which are strewn all around us. In times where large-cap companies have shrunk to become mid-caps and maybe even low-caps, you might be surprised how much of a good stock only a little bit can buy. Shelve that party you’ve been planning. Buy a good stock instead!

What if the markets go down more, much more? Well remember Mr. Buffett’s distinction between Price and Value. Price is what you give, Value is what you get. If something worth $1 is available for 50¢, should you defer the purchase in the fear that the next day it MIGHT go down to 25¢? Well, is there any rule that says that if a company is going for free (eg. A debt free company where market cap = or < cash on the books) it cannot go for a higher discount? No such rule that we are aware of, though it would be reasonable to presume that at some point in time such a company (in a simplistic scenario) will become a takeover candidate. Or atleast the price will rise such that it ceases to be a free lunch.

Further, do remember that India continues to be largely a domestic story and the only question is whether the growth will be closer to 5 or 6 or 7%. And yet, hidden somewhere in the macro country level PE ratios, are companies that are going for free, with dividend likely to be continued and maybe increased. Or with likely growth figures likely to be far higher than the much quoted GDP growth figures. Investments made now will, as one of our American friends has commented, make many millionaires and billionaires of the future.

Brevity of memory is not a problem only for the speculative times, it works with equal force during the bad times also. Our suggestion: stop worrying about whether we have reached the bottom, let it run its course like it always does. Keep moving through the sand and the snow towards the oh-so-far-far-away promised land. Meanwhile why look at the stock quotes on a daily or hourly basis? As Shrek suggests to Donkey, find something to keep busy. Well, maybe watch a few cartoon movies with the family.

{kind=link}